There are many great reasons to work with a mortgage broker when you are buying or refinancing a home. Your mortgage is likely to be your biggest financial decision you will ever make, so it is crucial to understand just how valuable your mortgage broker is. Here are...

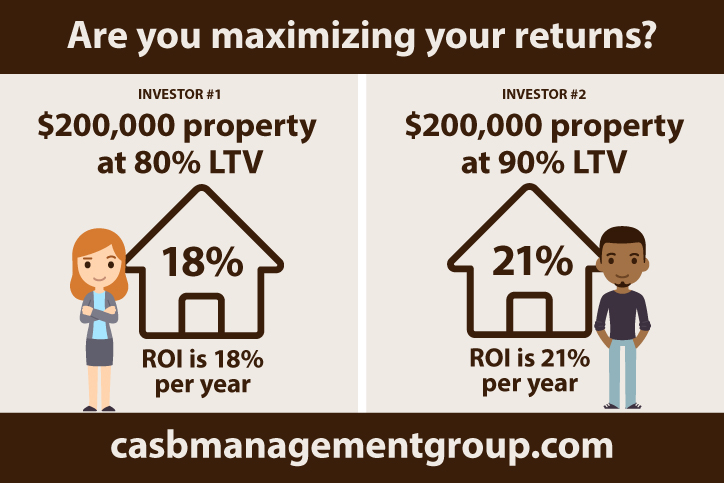

Private lending is a great tool to maximize real estate returns. Typically you can only finance up to 80% LTV (loan to value) on a rental property with traditional lenders. By adding additional mortgage debt through the use of a second mortgage, it is possible to...

Savvy real estate investors understand that to grow an investment portfolio, one needs to leverage their own financial resources, or in effect “use other people’s money” to expand. Savvy investors understand that by using leverage, you maximize the return on your own...

Real estate investors involved in house flipping projects often secure private lending. Perhaps they lack the renovation funds needed to complete the project. Perhaps they enjoy the ease of the private funding process. Private lenders use a “common sense” approach to...

Our client was unemployed with poor credit, but saw the opportunity to acquire a principal residence home with the down payment from an inheritance. Lack of income and poor credit would by themselves be conditions conducive to a private mortgage, but the kicker was...

People ask me about the type of private mortgage deals we fund and why customers would enter into a private mortgage arrangement over a more traditional bank mortgage. Private lenders lend using a “common sense” approach. Each application is considered based on a...

It’s time to get serious about saving for that ‘rainy day fund’ The global pandemic has reinforced the need for Canadians to take a more responsible approach to managing spending habits. The need for a savings pool that is not earmarked for a vacation or future spend...

Let’s consider your income, credit, down payment, liabilities, pre-payment options, pre-payment penalties, mortgage restrictions, portability, assumption options, amortization, age, location, rents, and more. Wait, what was your question? Your goal is to obtain the...

You are buying your next house. You ask your realtor what their role is in the process. 9 out of 10 realtors will give you these two standard responses; “My role is to find you a house that meets your requirements and negotiate the best price for you”. (Don’t take my...

The COVID-19 pandemic has shone a spotlight on what we have known for some time. As a country, Canada is unprepared to house and care for an ageing population. Waiting lists are now months if not years, to get a spot in retirement and nursing homes. Not enough new...

No, you don’t get 6 months of mortgage forgiveness during the COVID-19 crisis. I am fielding many calls during the current COVID -19 crisis from clients who are assuming they don’t need to pay their mortgage for the next six months, at no consequence to...

Refinancing a mortgage is inevitable for most people who own a home. Are you guilty of one or more of the following mistakes? Accepting the written offer your lender presents to you Lenders are famous for sending a renewal notice in the mail and asking you to select...

When the Government of Canada introduced the First Time Home Buyer Incentive (FTHBI) effective September 2, 2019, I expected more buzz in the mortgage community. The program is available to first time home buyers with household income under $120,000 for mortgages not...

Since cannabis legalization came into effect on October 17, 2018 nationwide, many Canadian landlords are wondering about their rights and how the legalization will affect their rental property investments. New rules allow cannabis to be used recreationally and enable...

When you think of what you look for in a mortgage, was rate the first thing that came to your mind? It is the most common feature of a mortgage in which we all focus on. But is it truly the most important? Let’s explore the features of a mortgage and why they are all...

When it comes time to purchasing a home, do you choose the more expensive but brand-new home – or do you go for that fixer upper with the potential to become your dream home? In order to make this important decision, you will need to consider if renovations are a fit...

Using mortgage prepayment options can drastically reduce the total amount of money you spend on your mortgage – and shorten the time it takes to pay it down! If you follow these three steps, you can be mortgage free sooner than ever! 1. Know your prepayment privileges...

With the increasing stricter mortgage regulations in Canada has prompted the question, if you have to file bankruptcy is a mortgage still attainable? Most Canadians think of this as not possible, but let’s review what bankruptcy is and how you can rebuild your credit...

What is an appraisal? Simply put: an appraisal is a professional’s opinion on the true market value of your home. Banks use appraisals, and so do home owners during the process of buying, selling or refinancing a home. How do appraisers calculate my home’s worth?...

Guest blog: Bruce McLennan, McLennan & Company Limited This is a common question and one that we often hear: What is the difference between a consumer proposal versus bankruptcy? Last week, we talked about your options in securing a mortgage if you file for...

Increasingly stricter mortgage regulations in Canada have prompted the question: If you have to file bankruptcy is a mortgage still attainable? Most Canadians think of this as not possible, but let’s review what bankruptcy is and how you can rebuild your credit score...

I had the pleasure of attending a conference recently where Michael “Pinball” Clemons was the guest speaker. You may remember Pinball as the Hall of Fame football player and coach with the Canadian Football League’s Toronto Argonauts. He is a multiple Grey...

Today’s buyers have almost an unlimited number of mortgage financing options to choose from. If you cut through all the marketing hype, you are going to be essentially selecting from one of three options: 1. Fixed rate mortgage, where your interest rate and payment...

Many Canadians are looking at holding mortgages well into retirement and are concerned that once Canada Pension and Old Age Security become the primary source of income, they may no longer qualify for a mortgage. For those of you in that position, I have some good...

We have witnessed three quarter point interest rate increases since July of 2017, with the most recent occurring on January 17, 2018. More increases are expected in 2018. If you own a home or are purchasing a home why does this matter? The price is not the price The...

On the surface, reverse mortgages seem like the ideal solution for cash-strapped seniors. At age 55 you can tap the equity in your home up to 55 per cent of the property value; you don’t have to make any interest or principal payments, and the mortgage only...

When renovating a home there are a number of financial strategies that can be used depending on the cost and timing of the renovations and whether the home is owner-occupied or a rental property. ...

With escalating home prices in cities such as Toronto and Vancouver having a residual effect be felt across much of the country, many Canadians are looking at holding mortgages well into retirement with no hope of actually paying them out once Canada Pension and Old...

NO WORRIES, THERE ARE THREE OTHER LENDER TYPES AVAILABLE Being turned down by what we call a traditional lender or “A” lender such as a charted bank, is not the end of the road in terms of your search for a mortgage. There are three other options available...

Using the services of a mortgage broker helps with both Purchasing a home is an exciting time. A lot of research goes into the purchase process, but we find many clients spend little time researching the best way for them to pay for the property and simply accept the...

Have you ever thought about using real estate to increase your overall net worth, or as a way to save for your retirement? Or even as a retirement plan instead of a traditional RRSP? You’re not alone, as we can tell from the Statistics Canada’s numbers from...

How Do I Check My Spouse’s Credit? According to the BMO Wealth Planning Group, close to two-thirds of married Canadians wish they had spent more time discussing their financial situation and plans for the future with their partner before getting married. I...

As fall moved into winter, real estate market in London cooled considerably from the buoyant spring and summer market with sales levels lower than 2016 for the past two months. Make no mistake, 2017 will be the all time best year for London real estate, but is this...

January 1, 2018 will bring another change to mortgage rules that will apply to all federally regulated financial institutions. The changes are to reinforce the expectation that lenders will remain vigilant in their mortgage underwriting procedures. Currently all...

These are interesting times for London real estate. A good time to sell in response to increasing demand and increased selling prices. 6,295 residential homes have been sold in London and the surrounding area during the first seven months of 2016. Sales are on pace...

According to a recent survey conducted by CIBC, 26% of Canadians consider paying down debt and keeping up with their bills to be their top financial priority in 2016, for the sixth straight year. (Source: Business News Network) As debt continues to be a concern, it...

At the beginning of each year, millions of people set their New Year’s resolutions. However, the large majority of people break their resolutions. Instead of setting vague, huge resolutions, you might want to try setting very specific goals and making a plan of how to...

I reviewed the London Free Press article recently allowing Granny flats in the city and the proposed impact on housing near the post secondary schools. (London to debate granny flat demand http://www.lfpress.com/2015/11/22/london-to-debate-granny-flat-demand). The...

as seen in the December 10th issue of the Londoner http://eedition.thelondoner.ca/doc/The-Londoner/the_londoner-1210/2015120801/#24 The London-area real estate community is breathing a sigh of relief after the announcement by Municipal Affairs Minister Ted McMeekin...

I recently read an article by Adam Mayers in the Toronto Star. The subject was Arlene Dickinson, best known as one of the tough-talking, no-nonsense venture capitalist co-hosts of CBC’s Dragon’s Den. When she was asked what her biggest life lesson was, she responded...

Calculating the economic impact of tightening mortgage rules by Bruce Smith It’s harder than ever for those who are self-employed to qualify for mortgages because of changes made over the past five years. These changes to the mortgage rules have been implemented by...

I have been very interested to see the polarization in London about the possibility of City Hall’s acceptance of Uber, with the service being adopted in the city without consequences. For the uninitiated, Uber allows consumers to request rides via a downloadable app...

I was reminiscing about my first home purchase, a two bedroom, 1.5 story home in Toronto in 1983. I was a 21-year-old full-time university student at the time, but the prospect of paying rent for another year did not make much sense to someone enrolled in a business...

It has now been two weeks since the most recent .25% cut to the Bank of Canada’s overnight rate. My question is “What is the impacted to you and your mortgage?” 1. Despite the .25% reduction, the Prime Rate in which banks lend money, only reduced by .15%. This is the...

This article written by Bruce Smith was originally published in The Londoner’s May 14, 2015 issue. Starting your own business is the dream of many Londoners or, for that matter, many Canadians and others around the world. You have an “idea” for a business, a...

This article was originally published in the March 26th, 2015 edition of The Londoner, which is available online here. Bruce Smith, Special to The Londoner It seems that not a day goes by without another media report on the amount of personal debt carried by...

Many start up companies need to raise capital to grow or expand. One method may be to secure “Angel Money”, amounts typically in the $25,000-$100,000 range, from an angel investor. Entrepreneurs can find this challenging, largely because they make one or more of the...

In preparation for a lecture on crowdfunding to a group of accountants, I discovered from my research of that the concept of having many people invest a small amount of money into a company, is more myth than fact. Sophisticated investors are unlikely to forward $1000...

I was reading an article by Carol Roth on this subject and was immediately intrigued by her assertion that one of the most counter-intuitive traits that can hurt entrepreneurs is smarts. In summary: While you may think that being smart, motivated and talented would...

Refinancing your home can seem daunting; there may be a penalty to pay out early, and you’ve been working hard to reduce the amount you owe on your mortgage. So why do it? Whether you need cheap money for home renovations or are looking to take advantage of a...

Why use a broker? It’s a question I get asked from time to time, often from those who went directly to their bank when they bought their property decades ago. The mortgage landscape has changed since then, and the terrain can be difficult to navigate. That’s where...

Everyone has needs unique to their financial situation. Accordingly, there are many kinds of mortgage, designed to fit those needs and give the client the solution they deserve. Here are five mortgage products that you may not have known about. Business for self –...

According to a survey conducted by the Canadian Payroll Association, Canadians have poor saving practices and are prepared to work longer to make ends meet. This mirrors the common belief that the children of baby boomers will have a poorer standard of living than...

I wrote the above article and was pleased to see its inclusion in the August 7 edition of The Londoner. In the end, entrepreneurs need to be able to access capital: hopefully you find these tips helpful when you approach investors with a business plan of your...

Casb Management Group Inc. provides private mortgage funds with a primary focus on residential properties in London, Ontario and the surrounding area. As a “common sense” lender, each application is considered based on a combination of income, credit and equity....

Given the volatility in the stock market and low returns experienced with fixed income instruments, many investors are seeking alternative investments that provide an attractive rate of return with an acceptable level of risk. When investing in mortgages you are...

Lenders and entrepreneurs have different perspectives and different interests. These differences are ingrained, but good financial times can create a comfort level that obscures them. Now in times of tighter credit and a slower economy, these different interests are...

The Canadian Mortgage and Housing Corporation (CMHC) is moving yet again to tighten the home mortgage market with changes that will make it more difficult for certain Canadians to obtain government-secured financing for real estate purchases. We will seek further...

According to a BMO poll released on April 16, 2014, 64% of Canadians would rather talk to the kids about sex then they would about money. This would indicate that the majority of parents acknowledge that they simply are not equipped to provide proper financial...

Colleague David Grossman posted this list and I am in full agreement of as to how I think a mortgage broker or agent should engage his/her customers. • Thou shalt not charge exorbitant fees • Thou shalt not push a borrower into a mortgage they cannot afford • Thou...

Now that we have entered the month of April, we rapidly approach the deadline for filing our personal income taxes. I believe there is a direct correlation between how you file your taxes and the overall type of person you are. This is strictly a theory, but my life...

As a real estate investor, I have always subscribed to the old adage that any time is the best time to purchase real estate. With that said, springtime is my personal favorite, as both buyers and sellers emerge from hibernation; show shovels replaced by sun showers...

Mortgage loan insurance, an insurance put in place to help protect lenders from mortgage default, is typically required by lenders when homebuyers make a down payment of less than 20% of the purchase price. Effective May 1, 2014, Canada Mortgage and Housing...

I recently met with a colleague in the mortgage industry. He was discussing the pitfalls associated with being the leader of his team, the need to constantly be “the guy” to make things happen. I could sympathize, as I share the same concern. The time and energy I...

With the 2014 Olympic Games commencing in Sochi, we can again look forward to inspirational performances that demonstrate perseverance, overcome seemingly insurmountable obstacles and inspire us to what is possible. Here are a few of my favorites moments from past...

All parties – bankers, lenders, mortgage brokers — have a responsibility to perform due diligence with every valued client we deal with. However, there is one step that is either overlooked, or not valued, by some folks in this business. It is a step that I feel...

In its latest forecast for the London, Ontario real estate market, CMHC projects a balanced market for 2014 driven by the first-time buyer market of the Echo Boomer generation currently the age 19-31 demographic. First-time buyers typically drive any real estate...

With the right resolutions and mindset, 2014 will be your most successful year in business. Combining a recovering economy with your own skills and mental toughness, this could be the year to make your dreams a reality. Need to refocus to make this happen? Here are...

Inspired by Matthew Ross, we look at five common problems facing entrepreneurs that don’t involve financing: Time constraints The scarcest of recourses is time. Time spent making the next sale or managing the day-to-day activities (working in the business) leaves...

It was my pleasure to speak at the November 4 event. My topic, “The Top 10 Considerations For Owing Your Own Business,” provided the audience the framework in which to select the appropriate opportunity for them based items such as interest, need, growth, skill set,...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So my last few...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So my last few...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. My last few blogs...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So my last few...

Buying a home – finding it, financing it, insuring it, and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So my last few...

Establishing credit is a critical undertaking, and one of the most important things you need to establish early in your adult life. Good credit makes it easier to purchase a home or vehicle, obtain insurance or, in some circumstances, find employment. Here are five...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So my last...

Buying a home: finding it, financing it, insuring it – and all the other steps involved – isn’t a simple process. Helping you understand that process is part of my job as a mortgage broker, and this blog brings you info you need in bite-size pieces. So, my last...

Teams are the way to go. The Ravens are a team; they won the last Super Bowl. The Prime Minister’s Cabinet is a team; they run the country. The astronauts are a team on each launch; they successfully negotiate space/the moon/the space station. Whether it’s...

Teams are the way to go. The Ravens are a team; they won the last Super Bowl. The Prime Minister’s Cabinet is a team; they run the country. The astronauts are a team on each launch; they successfully negotiate space/the moon/the space station. Whether it’s football,...

Teams are the way to go. The Ravens are a team; they won the last Super Bowl. The Prime Minister’s Cabinet is a team; they run the country. The astronauts are a team on each launch; they successfully negotiate space/the moon/the space station. Whether it’s...

Teams are the way to go. The Ravens are a team; they won the last Super Bowl. The Prime Minister’s Cabinet is a team; they run the country. The astronauts are a team on each launch; they successfully negotiate space/the moon/the space station. Whether it’s football,...

We love creative financing solutions and one became a reality this year: creating a new financing loophole or closing a loophole, depending on your perspective. Under current lender guidelines, you can refinance your current home to a maximum of 80% of its appraised...

I have been searching for a financial planner for quite a while and have been surprised if not shocked on how difficult the process has been. I don’t think my needs are unique. I am seeking someone with an A-Z understanding of all the investment options available to a...

To build a successful business, entrepreneurs need to invest a lot of time and energy in their work. This often results in a lack of exercise, sleep and a poor diet which ultimately leads to wear and tear on the body and mind and could lead to serious health issues....

In this current economic environment, we continue to manage our growing portfolio of clients and are capable of assisting companies even under the toughest circumstances. As our economy continues on its journey through the current re-alignment, we are actively...

So you want to be a real estate investor? Here are the top 5 mistakes made by investors old and new. 1. Not conducting adequate due diligence Purchasing an investment property is all about profit, maximizing revenue and minimizing expenses. Verifying the...

During November each year Movember is responsible for the sprouting of moustaches on thousands of men’s faces in Canada and around the world. With their “Mo’s “ these men raise vital funds and awareness for men’s health, specifically prostrate cancer and male mental...

When interest rates are low, it is traditionally a great time to borrow funds using your home as collateral, with little concern for paying off a mortgage. A great time to access cheap money for alternative investments, by essentially leveraging the equity in your...

A joint venture (JV) is a business agreement between two or more parties who seek to join alliances for the purpose of creating a new business entity or cultivating a new idea. Ideally each party brings a unique skill set to the mix, exercises control over the venture...

Over the past couple of months we have seen a gradual shift in mortgage rules most notably; The end of 100% financing and the cash back mortgage The reduction in line of credit limits to 65% of the home’s value compared to the previous 80% What makes this round of...

I heard this line from author, salesman and motivational speaker Zig Ziglar at a live seminar and immediately identified the premise to be true as a direct contradiction to the traditional teachings of business coaches that people do business with people they know,...

“Wouldn’t it make more sense if the deposits and borrowings were combined? Why not have every dollar you earn paying down your debts until you need to spend that money? Your income can instantly reduce what you have borrowed. As you pay bills and other expenses...

Inspired by the teachings of artist and writer Jessica Hagy, I recognize that nothing incredible is accomplished alone. You need the help of others, and with the right mix of talent on your team, the impossible becomes inevitable. Are these people on your team? The...

Regardless of your political views, I think we can all agree that the election of Donald Trump is going to bring “uncertainty” to the Canadian real estate market, both from a global perspective and with possible trade tariffs. The world as we know it is going to...

The last several months have seen a change in Canadian mortgage rules to stimulate a stagnant housing market. We have summarized below:1. The threshold for mortgage insurance has risen to a $1.5 million purchase price. 5% down on the first $500,000 and 10% down on the...

2023 was a bad year for mortgage renewals. 2024 and 2025 will be worse.If you experienced a mortgage renewal from a 5-year fixed rate mortgage in 2023 you would have experienced about a 20% monthly increase in payments. This may have resulted in some pain; a...

It’s crucial to be mindful of your finances and find ways to save money. Here are 12 tips to help you save during these challenging times: 1. Create a budget: Develop a comprehensive budget that outlines your income and expenses. This will help you understand...

Please Note: Our Centum affiliate produced this article on investing strategies. Enjoy. Real estate investing is like a big game of Monopoly, except instead of plastic hotels and paper money, you’re dealing with real properties and actual cash. It’s all...

Regardless of your position on the war in Ukraine, beyond the appalling human destruction and suffering that has occurred, the Ukraine war was lost before it began for all concerned. Regardless of the military outcome, a change has occurred in the world order that...

If you own a home, have a mortgage, or want to purchase or sell a home, the upcoming higher interest rates are going to impact you in some capacity. This is just the start of what is about to come in 2022 so now is the time to review and take action if required.1....

Recent Comments